Net Worth Update – £138K – Oct ’23 (Down £1,573.49)

If you are new here I update this blog with my net worth each month, tracking my progress to financial independence. Like many chasing FIRE (Financial Independence Retire Early) I mostly chasing this so I can focus my times on things that I love.

To see how I got started you can look at all my net worth posts here: https://growingmoneytrees.org/net-worth/

The closer you are to being non-reliant on your day job the more risks you can take, the more skills you can learn, or art you can produce. I love this idea. Whilst I am still trying to do as many thing as I love whilst I am young, I like to look at my life through incremental progress and the net worth number is a good way to do this.

If you’d like to follow along you can follow my newsletter here:

October:

This is really for the month of September, I do the reflection at the start of the month. I can’t quite remember when this got pushed but anyway!

I thought I would have made a bit more progress this month, and to be fair, I would have done if it wasn’t for house prices starting to crash. As I track based on the median price on Zoopla (I know, these are almost always too high), I had to write down my equity by £3k this month. Without which I would have increased my net worth by (quite typical) £1.5k.

Hey – If you want to read some oldies to see how I got started, then click below:

- Net Worth Update for March 2021 – £51,951 (+£5,423)

- Net Worth Update for April 2021 – £67,028 (+£15,077)

- May Update – £70,976 (+£3,948.00) – Total Restricted/Unrestricted Wealth = £85,579

- Net Worth Update – August 2021 – £81,385 (+£6,607) month over month

- December 2021 – Net Worth Update: £100,543 – The First £100k is the hardest!

Property:

I’m quite glad that my net worth is becoming less reliant on my property price. Property value really does not give me much, and I am more than happy for them all to crash by 30%, it makes no different to me. If it makes life easier for all then I am happy. I know there are plenty of people with much less equity who will be hit, badly, so there is no good answer. It’s all a bit of shambles at the moment. Currently my equity is: £117k – which still makes up 85.38% of my net worth – ridiculously high I know! But it used to be 99% 3 years ago, so I feel this is pretty good progress.

Balance Sheet:

- RSUs: £4,500 (down £500) – only those vesting this year

- Monzo: £1000 – flat I only keep living expenses here

- FreeTrade Shares: Remain at £371

- Savings : £1915 (split between Santander 5% easy access, and NatWest Digital Saver – £150 per month)

- Trading212 – £3448 (started dripping savings into here at £5 a day, and a £150 a month)

- Pension: £15,500 – Around £500 a month going in here (going up next month) from myself and employer, could probably afford to put a bit more here, but there is some much uncertainty at work I’m keen to keep more powder dry

- Debt: -£6319 – fixed at 1.7%

Income:

- Ezoic (blogging): $3.24

- NatWest: £5.67

- Medium: £0.21 (just started!)

- Chip: £2.45 (now moved to Santander)

- Stock Income: £3.90

- Other: $7.67

- Total: £19.23

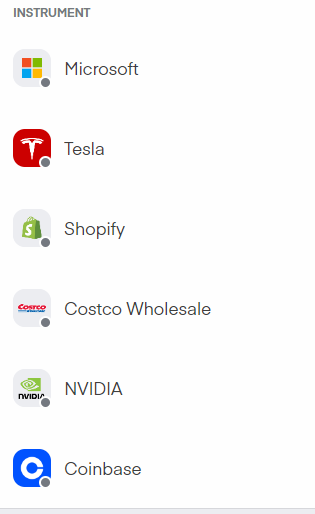

Not a bad month, starting to generate some cash from a few different places. I’m not actively investing for income but a few of my stocks happened to pay out this month. I’ve literally just altered my portfolio whilst writing this to mostly focus on bullish plays, and very few of them. Below is the pie:

I am bullish on all of these, Microsoft and Costco are my “Safe Bets” that should keep the portfolio going upwards. The others are bets on big things, Coinbase ($COIN) is cheap, Nvidia is not. Tesla is somewhere in the middle. I will have about £2k in this when market opens, and will be adding min. £5 a day to it (might up to £10). And my UK portfolio made up of City Pub Group (My Justification is Here: Last Time This Stock Was Tipped It Went Up 40%) and Games Workshop (GAW). I buy weekly (£25 a week). Total investment per month is £250. Which currently seems sensible but will see what the next few weeks brings us.

Niche Sites:

Google brought in an update on Google Search which changed how people find pages in Google. It was a big move. So far it seems like “actual” business and people who are genuinely interested in their topic are doing well.

This blog is a perfect example, I get a little bit of traffic from Google and other search (around 100 per month). So far I have increased my rankings rather than dropped down. But my other site that is simply a project to try and make money has faired very poorly (from 50 impressions a day to 0). I thought I had written quality content but alas I had not!

Overall a solid month, if you read this far you might want to consider getting this monthly update sent to your email address by signing up below:

Keep Reading for Previous Months Updates:

- Net Worth Update December 2024

Finished the year without much of a bang, in total I reached £138,949.26 which is about a £1472 increase from last month, and an increase of 14k year on year from December 2022.

Want to follow my journey, get all my updates each month:

For those that are new here. I am Seaward, a 28-year-old living in the UK. Trying to be independently wealthy ASAP so I can focus on the things that bring me more joy. I still have a lot of fun and am not super frugal. Optimizing tax savings, and income rather than being frugal all the time.

Home equity still makes up the vast proportion of my net worth but it has been coming down in recent months. It currently stands at 83.77% (down from 90% at the end of December 2022). The single biggest factor in my net worth has been house price fluctuations. So with them declining slightly (on paper) this year, I am pretty happy that my net worth has improved and steadied over the last few months.

The biggest developments, for the first time in a while, have come from my income increases. It’s hard to track exactly but next year I should make a net income of at least £40k in 2024 which is equivalent to around a £60k gross salary (despite my actual income being around £48k). This is because I “rent a room” to my girlfriend who now lives with me. She gets very cheap rent, and this helps me save more (she also saves more now than she did in rented accommodation – her “rent” is very light for the area!).

The above excludes income from bonuses and RSUs, which should be around £5k gross this year. Bonuses are rare at the moment.

This ALSO excludes income from savings, dividends, blogging etc. Currently, these are minimal (around £100 a year), but I hope to balloon this to be worth at least one day of “normal” work. I’ve been trying a lot of things this year, and plan to sit down and focus on one or two that have worked well for me. This blog is really about documentation rather than any “real” money. Although I have heard of finance bloggers making a lot of money, I’m not sure anyone wants to hear from me.

Combining some of my finances with my partner, and talking to her about them, has been a revelation. You can read more about this topic here: FIRE Update – December 2022 – £124k – (Joint Finances and Life Changes) Working together makes the whole game of life a lot easier. It can be done as a single person, but the system is set up for a team of 2 or more.

Goals for 2024:

For 2024, I want to get this number to £166k, around a 20% increase. Even with house prices staying static, this should be achievable. I want to compound at close to 20% for as long as I can. I didn’t manage it this year, unfortunately (11%).

But if I can, I can follow the below chart:

Returning 20% a year is going to be tough in the future when I can’t just save my way there. House prices are unlikely to rise at that kind of rate, so I need the rest of my assets to compound fast or save/earn a lot more. Realistically it’ll be a combination of them all. They say the second 100k is easier than the first, but those people were living in a bull market.

My main concern is the cost of my mortgage going up with interest rates as they are. I could lose 200-300 a month in net cash. That’d hinder my life significantly.

Signing off for 2023. Good luck to all my readers in 2024. May they be healthy and prosperous for you and your loved ones.

Want to follow my journey, more blog posts below:

- Net Worth Update – November £137,387.68 (-0.5%)

Not the prettiest of months, I had to write down my RSUs (which also vest next week and I will be paying tax on!), due to my company being at a 5 year low. Bit of a tough one as I was hoping these RSUs would give me the cash buffer I could do with at the moment. My net worth has been stagnant for the past few months, but given the decline in stocks and house prices I think I have down well to cling on. When the bull market returns I expect to do very well.

Life: There has been a lot going on in my life with the birth of my first nephew and various drama. I ran my first half marathon in a time of 1.55 which is reasonable I think… not quite the 1:45 I wanted but I definitely did not train enough for it. My mental health has been “ok” but not marvelous. Mostly because I hurt my foot and could not run. It’s amazing the effect of not being able to do the thing you rely on for your mental health. All my other habits didn’t happen nearly as often as they should have done once I stopped running. I need to diversify the tools I use for my mental health, mediation, singing anything really.

Portfolio: £3450

I changed my strategy for my Trading212 investing account as I decided I wanted to be much more ambitious in this portfolio. My risk tolerance is very high, and I have plenty of exposure to S&P in my pension (I changed from the Scottish Widows North American Fund to an actual S&P one, I hadn’t realized the fees were so high on the former (0.8%!) which will save me a lot in the long-run.

I bought two quite ambitious and risky stocks this month (and consolidated all my investments into these two) Oxford Nanopore – I bought just after they were mentioned in Apple’s M3 chip launch hoping for a bit of a trade. I’m up about 6% in a week but I think that is from sentiment turning around within sequencing. PacBio massively outperformed expectations so the sector has turned, momentarily at least, bullish. The second company I bought this month is Oxford Biodynamics Plc as they roll out their new prostate cancer test in the US and UK. Currently neither are profitable, but the amount of growth potential (and actual revenue sales) is outstanding. I’m very much looking forward to seeing how they fair.

Rest of the balance sheet looks like this:

- Pension: £15500

- Crypto: £700 (staked Ethereum)

- Savings £1884 (NatWest Digital Saver and Santander 5%)

- Home Equity: £118,000

- RSUs vesting 2023 – £2800 (subject to tax on vest)

- Stocks – £3450 and £371 left in FreeTrade (via Crowdcube)

My girlfriend and I have reached an agreement for me to focus on my side hustle at certain times of the week, and she is going to help hold me accountable. I’m still debating which of them I want to go “all-in” on but I’m seeing some good traction on Google for one in my professional and local niche, which I think would be well worth fleshing out.

- Net Worth Update – £138K – Oct ’23 (Down £1,573.49)

If you are new here I update this blog with my net worth each month, tracking my progress to financial independence. Like many chasing FIRE (Financial Independence Retire Early) I mostly chasing this so I can focus my times on things that I love.

To see how I got started you can look at all my net worth posts here: https://growingmoneytrees.org/net-worth/

The closer you are to being non-reliant on your day job the more risks you can take, the more skills you can learn, or art you can produce. I love this idea. Whilst I am still trying to do as many thing as I love whilst I am young, I like to look at my life through incremental progress and the net worth number is a good way to do this.

If you’d like to follow along you can follow my newsletter here:

October:

This is really for the month of September, I do the reflection at the start of the month. I can’t quite remember when this got pushed but anyway!

I thought I would have made a bit more progress this month, and to be fair, I would have done if it wasn’t for house prices starting to crash. As I track based on the median price on Zoopla (I know, these are almost always too high), I had to write down my equity by £3k this month. Without which I would have increased my net worth by (quite typical) £1.5k.

Hey – If you want to read some oldies to see how I got started, then click below:

Property:

I’m quite glad that my net worth is becoming less reliant on my property price. Property value really does not give me much, and I am more than happy for them all to crash by 30%, it makes no different to me. If it makes life easier for all then I am happy. I know there are plenty of people with much less equity who will be hit, badly, so there is no good answer. It’s all a bit of shambles at the moment. Currently my equity is: £117k – which still makes up 85.38% of my net worth – ridiculously high I know! But it used to be 99% 3 years ago, so I feel this is pretty good progress.

Balance Sheet:

- RSUs: £4,500 (down £500) – only those vesting this year

- Monzo: £1000 – flat I only keep living expenses here

- FreeTrade Shares: Remain at £371

- Savings : £1915 (split between Santander 5% easy access, and NatWest Digital Saver – £150 per month)

- Trading212 – £3448 (started dripping savings into here at £5 a day, and a £150 a month)

- Pension: £15,500 – Around £500 a month going in here (going up next month) from myself and employer, could probably afford to put a bit more here, but there is some much uncertainty at work I’m keen to keep more powder dry

- Debt: -£6319 – fixed at 1.7%

Income:

- Ezoic (blogging): $3.24

- NatWest: £5.67

- Medium: £0.21 (just started!)

- Chip: £2.45 (now moved to Santander)

- Stock Income: £3.90

- Other: $7.67

- Total: £19.23

Not a bad month, starting to generate some cash from a few different places. I’m not actively investing for income but a few of my stocks happened to pay out this month. I’ve literally just altered my portfolio whilst writing this to mostly focus on bullish plays, and very few of them. Below is the pie:

I am bullish on all of these, Microsoft and Costco are my “Safe Bets” that should keep the portfolio going upwards. The others are bets on big things, Coinbase ($COIN) is cheap, Nvidia is not. Tesla is somewhere in the middle. I will have about £2k in this when market opens, and will be adding min. £5 a day to it (might up to £10). And my UK portfolio made up of City Pub Group (My Justification is Here: Last Time This Stock Was Tipped It Went Up 40%) and Games Workshop (GAW). I buy weekly (£25 a week). Total investment per month is £250. Which currently seems sensible but will see what the next few weeks brings us.

Niche Sites:

Google brought in an update on Google Search which changed how people find pages in Google. It was a big move. So far it seems like “actual” business and people who are genuinely interested in their topic are doing well.

This blog is a perfect example, I get a little bit of traffic from Google and other search (around 100 per month). So far I have increased my rankings rather than dropped down. But my other site that is simply a project to try and make money has faired very poorly (from 50 impressions a day to 0). I thought I had written quality content but alas I had not!

Overall a solid month, if you read this far you might want to consider getting this monthly update sent to your email address by signing up below:

Keep Reading for Previous Months Updates:

- September 2023 Net Worth Update (+£2935.51)

This month was a long one, I feel like I achieved a lot of what I wanted to, and made some dents in my financial goals.

There is a lot below, including a total breakdown of my assets and liabilities, and my side hustles / projects that I am hoping will accelerate my towards retirement.

Want this sent straight to your email each month? Sign up below:

If you are new here, I track my net worth each month to shame me into keeping my spending and investing habits on track.

So far it has worked pretty well.

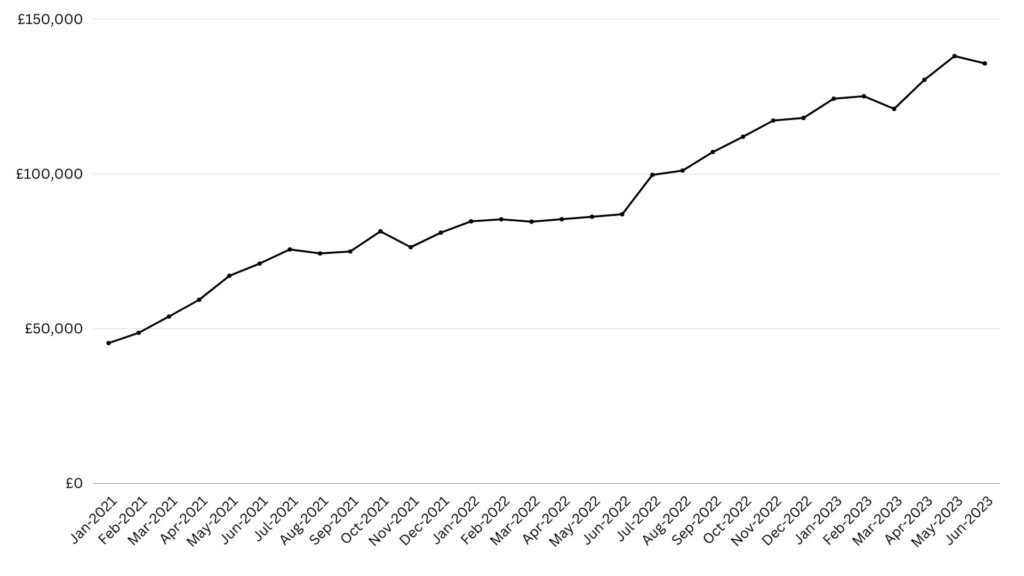

For September I reached £139,859 which is £2935.51 (2%) up since last month. Things are beginning to snowball… hopefully they remain this way as the economy dips.

Tracking My Net Worth

It’s broken down as follows:

Home Equity: £120,263 – house prices were flat, but I pay off around £600 in debt each month so this is a new ATH number (but not the highest house price). I expect this to come down a little in the future due to pressure on house prices, although because I bought at the lower end of the market I should be relatively isolated from this.

Balance Sheet:

RSUs (Vesting in 2023): £5,000

Shares in FreeTrade: £371

Savings: £2760 (Chip Easy Access at 4.84% and Natwest Digital Saver at 6%)

Trading212: £2,225

Pension: £14,700

Monzo Current Account: £1000

Debt: £6459

Moving forward I am considering upping my contributions to pension. I am likely to go into the 40% tax bracket this year, and my bonus (which is the main reason my NW has had a bump this year) was eaten alive by student loans.

Using salary sacrifice some of this money into my pension would seem the wise decision now I am on a fairly even keel. You can read my article on avoiding student loan repayments here: Does Salary Sacrifice Reduce Student Loan? With Video Explanation.

My current debt is the only thing I am worried about. I expect to surpass cash/stocks/savings of £6459 in the next couple of months, and it is fixed at 1.64% so I am not too worried. But for peace of mind, something I am optimising for a lot at the moment, this could be worth doing.

I shared a post on my twitter about the below chart:

“Why Earning Isn’t Enough – INVEST NOW,” I decided to tackle a topic that’s been on my mind.

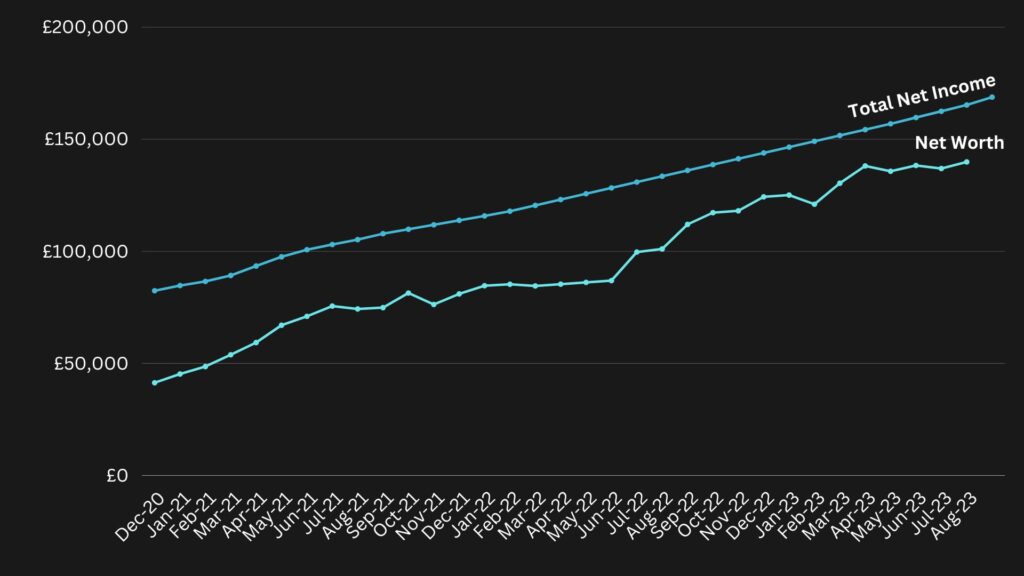

I shared the below chart that compares total net income to my net worth, something I’ve made a point to track meticulously since I started this financial journey.

Tracking My Net Worth vs Total Net Income What’s interesting is my growing confidence that my net worth is on the brink of surpassing my income, which is a significant milestone. It’s like the financial equivalent of saving 100% of my earnings over the past two years, all while disregarding day-to-day expenses.

Despite the unpredictable financial challenges we’ve all faced over the past couple of years, I’m proud to say that I’ve stayed committed to my investment strategies and remained focused on my financial goals.

There’s a saying that the initial 100k is the hardest to accumulate, and you can actually see this in the accelerating trend within my chart. Now, I’m eagerly waiting for that curve to turn parabolic, a moment I’m sure many of us anticipate.

Currently, I’m standing at 71% of my net income in my net asset column, although I must admit I’m not entirely certain when I’ll reach that significant milestone.

Side Hustles:

Blog 1 – this one, mostly left alone! Didn’t produce much income.

Blog 2: Spent many hours, now ranking for 11 keywords in Google, albeit a fair way down the list. Made its first cent the other day, (total $0.06 so far!).

This is just getting started, I am working hard and plan to grow it into a minimum $1,000 dollars per month business by this time next year. I am tweeting about it, and you can follow me here.

YouTube Channels:

YouTube 1: SEO focused – 3 videos + 1 subscriber (brand new) 7 views

Wildlife Niche Channel: 25k views, total 74 subscribers (mostly shorts)Personal Finance – 39 Subscribers (+5) and 471 views (mainly long-form)

Example video, you are welcome to subscribe if you’d like!

Undervalued Stocks UK Definitely spreading myself too thin but they all focus on different things, and don’t really want to mess up my algo with different content at the moment. The SEO stuff is quick to make, just doing short updates about my income etc.

- August Net Worth Update: £136,923 (Down by £1,362.49)

Hello, everyone! As we welcome a new month, it’s time to update you all on my financial journey. Even though August has seen a slight dip in my net worth, it has been a month full of learning and strategies for future growth. I am starting to see various side hustles tick up, albeit very slowly! Currently income from other sources is at £29 per month, I expect this to go up with the increase in savings rate. I’d like to get to the point where 30% of my income is from an outside source. Eventually of course, it’d be good to get a to 100% but baby steps and all that!

Uncertainty at work has finally been realized in layoffs within my team, I don’t yet know if I will have a job but either way I know I need to get smart about what I do with my spare time. I am building a few different things at the moment but ultimately I need to find what works and go deep on that. I love writing and would like to do much more of it. I think a personal writing style is going to become very important with rise of AI writers. I think the dust around this will settle eventually.

I’ve noticed a lot of Niche Site writers have switched or focused on travel sites, it makes sense given the climate. It’s very hard to replicate a good travel site with AI. Excellent content is king and we all need to be more cognizant of that. Whether I have the skill to compete in this arena is another thing entirely.

Here Is How it is Broken Down

Cash: £600

My cash position is lower then normal, but my and my partner have started setting aside our joint disposable income at the start of the month, so I am hoping this will pay dividends in the long run. Anything we don’t spend will go into our joint Monzo savings point. Which yields are 3.74% a little less than chip but the amounts are so small at the moment it’s not worth the complication of mixing them. Not until Chip brings out a joint savings account, now that would be great!

Shares: £371

The shares have been somewhat stagnant this month, but I am optimistic about their future growth. I am monitoring the markets closely for better opportunities to increase my holdings. These are just shares in FreeTrade via crowd funding. I now only hold pension funds and will be dripping into a vanguard fund in due course.

RSUs vesting in 2023: £5,000

Restricted stock units (RSUs) vesting next year will add a substantial amount to my net worth. This is something I am looking forward to as it will give a significant boost to my overall financial health. I am currently in talks around redundancy so it’s hard to say whether these will be forfeit or not. The package on offer is decent but I don’t expect to actually lose my job.

Savings: £4,254

My savings have been doing well this month. I have been disciplined in putting aside a portion of my income and reducing unnecessary expenses. This strategy is essential for my FIRE (Financial Independence, Retire Early) journey.

Pension: £14,263

My pension fund is an integral part of my retirement strategy. Its steady growth is a good sign for the future. I recently left FreeTrade and moved all my money to my workplace pension, this combined figure will be what is combined at the end of the week. It’ll be nice to have all my pension in one place, and start to accelerate my contributions. Currently, given my work environment, I am being more cautious than perhaps I would need to be normally, I want to ensure that I have as much cash on hand for opportunities (and in case I need it to survive!). My pension will need to be topped up, I am turning 28 this October and the amount in my pension is much less than it should be. I actually did have more but did some bold bets in my SIPP that did not quite playout. Lesson Learned! I can accelerate this fast as I am likely going to enter the top-rate of tax this year, meaning any additions will be even more tax efficient.

Home Equity: £119,649

My home equity continues to be my most significant asset. Even with fluctuations in the housing market, I am confident in its long-term value. I am very glad I bought at the start of the pandemic, you will notice from the graph above this has been a large contributor (for reference I put down £40,000 3 years ago). The compounded returns on money invested are significant even as interest rates climb. I bought a house that was one of the cheapest on the street and house hacked my spare room for a couple of years, I have various articles on this you can find here: House Hacking: A Global Guide

Household Debt: £6,600

We have a slight increase in my household debt this month due to some unexpected expenses. However, this debt is fixed at 1.64% interest so it’s not worth paying back (better to stick the same money into my savings account).

In total, my net worth is £136,923 for August 2023, which is a decrease of £1,362.49 compared to the previous month.

- June 2023 Update – £138k – And Why I Am Moving Away From FreeTrade

Subscribe to our newsletter!

As we find ourselves in the heart of summer, it’s the perfect time to take a step back and assess our financial journey. For those of us on the path to Financial Independence, Retire Early (FIRE), it’s crucial to regularly review our financial standing, make necessary adjustments, and celebrate our progress. Today, I’m excited to share with you my mid-year financial review, where I’ll be discussing my current net worth, my investment strategies, and some changes I’ve made to my portfolio.

The Current State of Affairs

Let’s start with a snapshot of my current financial standing. My house equity stands at a robust £120,035. This is a significant chunk of my net worth and a testament to the power of real estate as a wealth-building tool.

In terms of liquid assets, my current account holds £900, and I have £3557 in CHIP, a smart savings app that automatically puts money aside for you. I also have £757 in a NatWest 6% Digital Saver, a high-interest savings account that’s been a reliable place to park my emergency fund.

My investments in shares, specifically in FreeTrade, have been written down to £2.65 a share, totalling £371. Additionally, I have Restricted Stock Units (RSUs) worth £5000.

My pension pot is divided between a Self-Invested Personal Pension (SIPP) with £2700 and a Scottish Widows pension scheme with £11,200.

After accounting for a slightly expensive month and some investments coming down in value, my total net assets (excluding the house) come to £24,476, a decrease of £200 from the previous month.

The FreeTrade Saga

Now, let’s talk about FreeTrade. They decided to put their fees up at the worst possible time and, despite being user number 1000ish, I have decided to move on to more cost efficient paths. I will be moving my SIPP to Scottish Widows (for ease as my employer provided one and it allows easy ETF access at relatively low fees) and my ISA most likely to Vanguard, it’s currently being held in cash.

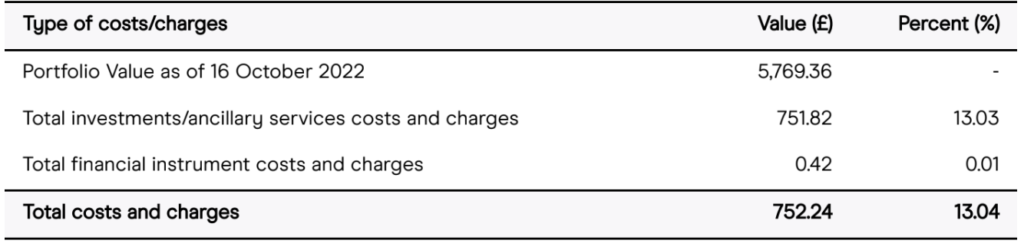

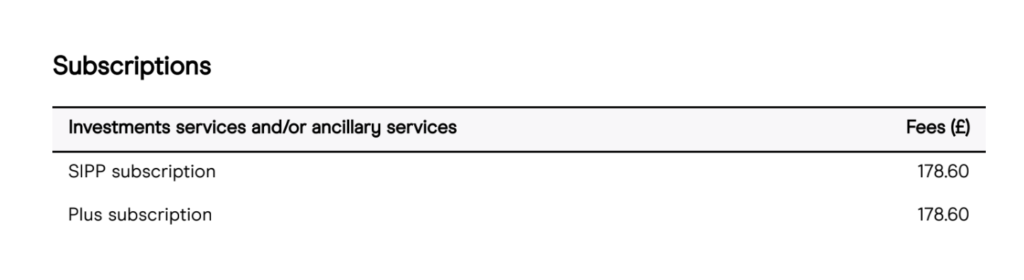

I don’t like being taken advantage of and the costs were already quite high to hold my SIPP their, with their 20% increase in fees I feel it’s time to cut my losses. You will see below that my costs were £752!

FreeTrade Fee Structure Decimates My Portfolio While I may have traded a bit too much, the subscription fee alone accounts for nearly £400! I thought FreeTrade were meant to help the little guy, but I feel more likely they are looking for older folks with bigger portfolios. It does seem a shame and I wish them all the best. I believe they could do more to engage with a fantastic community they have around them. But also appreciate times are tough, we all have to do things we don’t want to, but the same applies to me.

Below you will see proof of such costs:

FreeTrade Subscription Fees 2023 The Bottom Line

So, where does all this leave me in terms of net worth? After adding up all the numbers, my total net worth comes to £138,286. This is an increase of £2578 from last May, which is a solid step forward on my journey to FIRE.

In fact, this puts me at 27.66% of the way to my FIRE goal. While there’s still a long way to go, I’m proud of the progress I’ve made so far. It’s a testament to the power of consistent saving, smart investing, and the magic of compound interest.

Looking Ahead

As we move into the second half of the year, the financial landscape is riddled with uncertainties. The threat of redundancy looms large, and there are whispers of potential house price crashes. Despite the numbers in my net worth continuing to rise, the anxiety is palpable. It’s a stark reminder that the journey to financial independence is not just about growing our wealth, but also about managing risks and navigating uncertainties.

In these uncertain times, it’s crucial to stay vigilant, make informed decisions, and adapt our financial strategies as necessary. The path to financial independence is not always smooth, but with careful planning and prudent decision-making, we can navigate the bumps along the way.

Despite the uncertainties, I remain committed to my journey towards financial independence. The numbers may go up and down, but the goal remains the same: to build a secure financial future and achieve the freedom to live life on my own terms.

Stay tuned for more updates on my journey to financial independence. And as always, keep growing those money trees, even in the face of adversity!

- March FIRE Update – +26% YoY £130,380.67 (+£9,381.51)

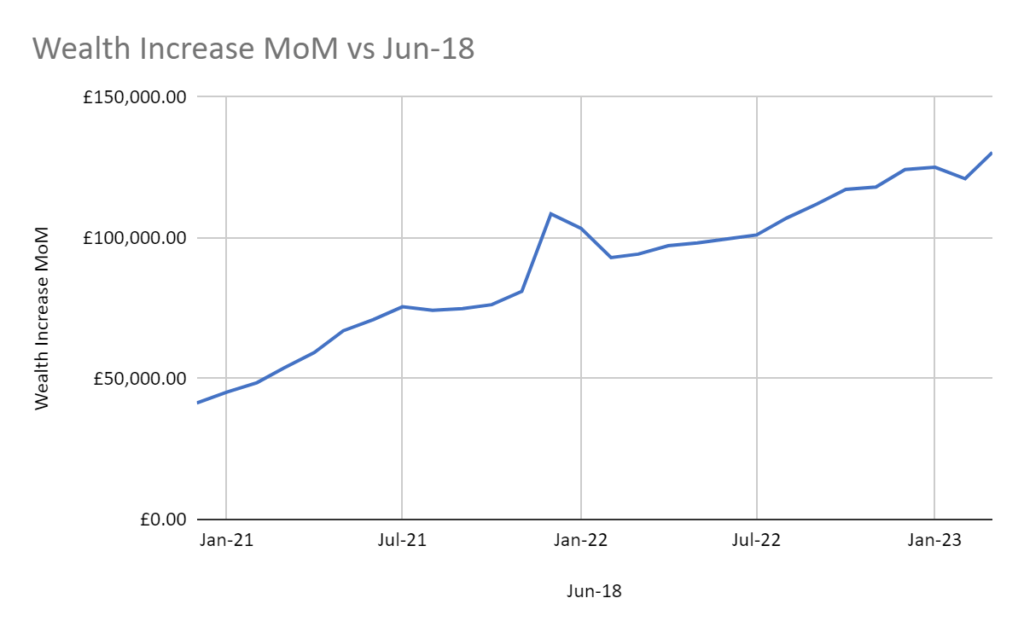

Well, when they said the first 100k is the hardest, they really meant it. Since February, I’ve added £9,381.51 to my net worth. This is roughly 26% to my FIRE target. This year it has been tough to make headway but even in one of the toughest years on record, my net worth has increased about 5% since the start of the year, with dips in house price and investment valuations. All things considered this is amazing.

When I look back to March 2022 my YoY increase is around £35,000 or 26%. If I can compound my net worth at this continued growth rate I will reach my goals much quicker than anticipated (1million in 10 years!). I suspect I may need to adjust my exact target depending on what my partner decides to do, and the kind of support she needs. It’s took me about 5 years of work to reach £100k, and yet it has taken me about 1 year to reach £130k. The compounding effect is really in full flow, and I’m not even earning over £50k yet.

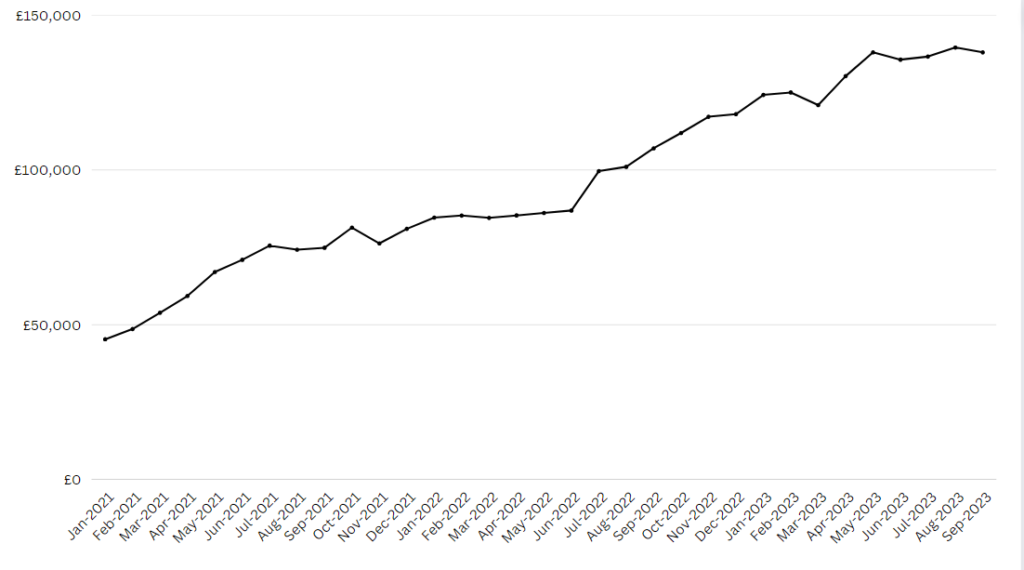

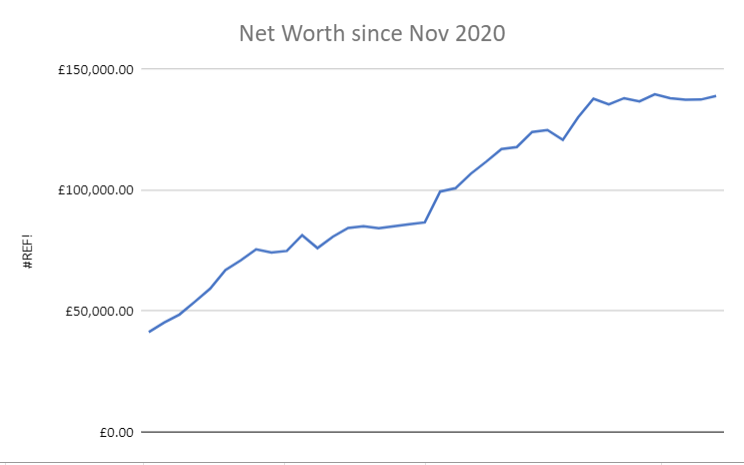

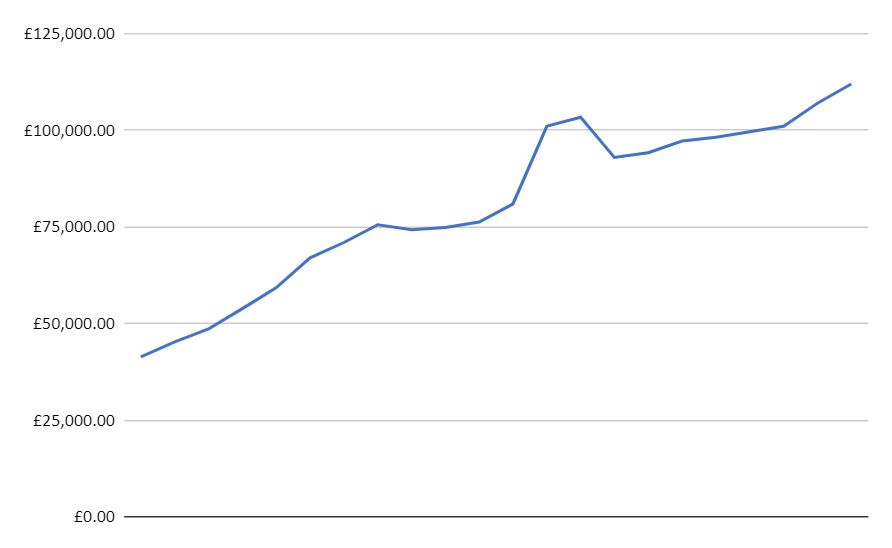

Here is my net worth overtime starting in Dec 2020 and finishing this month (March 2023). When you zoom out it looks smooth, but I promise you it is anything but that! I’ve felt pretty poor during this whole period, but managed to keep forward momentum and I am very happy with my progress. I’ve also managed to do a whole host of things, adventures, hobbies, and holidays so don’t feel I’ve missed out on much (if at all!).

These increase are attributed to:

- Pension contributions (reduced tax burden + employer contributions)

- House price increase (hopefully becoming less reliant on this as I will come on to later)

- Pay increases

- Side hustles (minimal so far)

- RSUs from work

- Cohabiting – reducing outgoings and partner contributions to house

I’m also very happy to note that that my net worth is made up of significantly less real estate (as a percentage) that this time a year ago. Partly, due to house prices coming down, but also mainly due to my other assets growing. This is welcome as I’d like to have options available to me rather than have all my money tied into my house!

Percentage of Wealth Stuck in my House Since Dec 2020 Ultimately, a good month in tricky conditions. I’ve budgeted better, exercised more, no drank alcohol, and manage to increase my NW by £9k. I feel no richer, but I guess that is the aim of the game!

I hope you are all doing well out there

- FIRE Update – December 2022 – £124k – (Joint Finances and Life Changes)

Why it was tough?

December was a tough month. Not only were the markets unkind to me (I have feelings too!), but it’s the most expensive month of the year. This was compounded by my decision to go skiing in the French Alps (cost over £1200) and buy very nice presents for the first Christmas with my girlfriend. I think for most people it won’t be news, I just so happened to also treat myself at the same time. I won’t make that mistake again.

There is always a temptation to splash out when you are in a new relationship. My girlfriend isn’t someone who is impressed by money, but we enjoy using our money on experiences that we will remember for the rest of our lives (hopefully together!). We’ve started to communicate much more clarity about our financial needs and burdens and it’s been great. In January so far we have drastically reduced our spending to pretty much only necessities. It turns out that when it’s too cold to leave the house we just cook with whatever we can find in the fridge. This has worked in our favour.

Talking About Money in a Relationship?

The real catalyst for us to discuss our finances in much more detail was my girlfriend saying yes when I asked her to move in. We’ve been talking about it for a while and we are very aligned on how we use our money, and how much she should contribute to the house. I don’t want to make a profit from her, but I also want her to feel like it is as much her home as mine.

We’ve agreed she will own no equity in the house, but I’ve agreed to a very modest monthly contribution from her that will leave her

a.) the ability to save (less than her current outgoings (rent +bills))

b.) give her a sense of safety, as if anything goes wrong she will be in the best financial position she’s ever been in

c.) we have a levelled our disposable income (just about) so we can plan holidays, investments and the like in a similar vein (this is after accounting for her increased savings and my having to pay the majority of the bills /mortgage (money I will get back when we sell)

The number we landed on was £400 incl bills. I pay around £1400 w/ bills a month so this brings my costs down to a more modest £1000. We have agreed that if the heating goes beyond x amount she will make a 50% contribution to the additional cost (which we both agree is fair).

So far, we have avoided joint accounts. We did try and onboard via starling back, but they rejected my application(?!), which I have to say is a first – especially for an online-only bank. We plan to just use split-wise for extra stuff and split everything 50/50. This is easy and simple, we can just settle things each month.

Once she joins me and all goes well, we will start planning our next move. With our joint income of around £80k, we could afford to move to something bigger, but that may not be the best use of our income. I haven’t mentioned the blog to her, not the exact FIRE topic. However, I have been clear in my life, professional, and financial goals (just not specifically mentioning what age I want to FIRE at).

This Months Numbers:

As of now, my current net worth is £124,565. This is made up of several different components:

- House equity: £111,300

- Credit card debt and other loans (Christmas and cashback): -£8,000

- Investments (including pensions and a Lifetime ISA): £20,265

- Cash and savings: £1,000

It’s important to note that my house equity, which is the current market value of my home minus any outstanding mortgages or other liens, makes up the largest portion of my net worth at 89% of the total. This is followed by my investments, which make up 16% of my net worth.

While it’s great to have a high net worth, it’s also important to keep an eye on your liabilities and make sure they are not becoming a burden. In my case, my credit card debt and other loans make up -6.4% of my net worth.

It’s also important to have some savings and cash on hand for unexpected expenses or emergencies. In my case, I have £1,000 in cash and savings, which makes up 0.8% of my net worth.

Overall, my net worth is a positive number, which is a good indicator of my overall financial health. However, it’s important to remember that net worth is just one measure of your financial well-being and it’s important to consider other factors such as your income, expenses, and overall financial goals when assessing your financial situation.

You can see the effect of starting to put more into my pension, my cash is low and needs attention, but I do have ways of raising money if I did hit an emergency. However, I will be replenishing my cash balance by reducing so of my pension payments and the extra £400 I will gain tax-free from my lodger, I mean girlfriend!

I’d like to get a minimum of 3month basic expenses, which I would put at £6k. I have a lot of work to do next year to get there. My loan is only 1.5% interest so not worth paying off in this current climate, I’ve got it going to work for me, although so currently a little underwater on it. I can take the risk as I am young and have assets to back me up if things get murky.

The reason I track all my money including mentions is that if I can get enough money in my pension (or project out what I will have aged 55) then I can work on my other investments. I would only need to survive 20 years from 35-55 if the pension was sufficient. However, given I’ve only been working 5 years and have not been perfect with how I have looked after my money, I consider myself to be on the right path.

If you’d like to see what I was doing this time last year, you can read here: https://growingmoneytrees.org/2021/12/29/december-2021-net-worth-update-100543-the-first-100k-is-the-hardest

In short, my net worth has increased to around £24k in a horrid investment environment. Mainly, this is due to house price appreciation, mentioned contributions and, as ever, a bit of luck!

I hope you enjoyed reading this, please do share the blog around and ask me any questions. All I seem to get is spam on here, it makes my heart hurt!

- October Net Worth – £118,069.63 (+1% / +£840) – 23.61% to FIRE

Not the most successful month, house prices seem to have stabilised, and I don’t expect many increases on this front (likely a sell-off in the short-mid term). Still, I am happy to keep forward momentum in a challenging macroeconomic environment.

I’ve increased my pension contributions to 15% of my salary and 10% from my employer, I am putting 25% of my income into the S&P. I want to treat myself as poor before I become it, so I don’t inflate my lifestyle. It’s a psychological trick. My thinking is this is an excellent time to dollar cost average, and I’d rather put the money in my pension for a few reasons:

- Reduce my tax liability (it costs my £300 in takehome pay to get £550 in my pension)

- Reducing my student loan liability (and interest rate that is triggered by a higher salary threshold)

- Pound-cost averaging in a down market, into a fund that I cannot sell for 30 years when the market returns in 2-3 years to a bull-run I will have £30-40k invested for the run-up

- This prevents me from panic selling if (probably when!) the market goes lower

- Should I happen to make outsized gains, I can reduce my pension contributions later in life when I need all the cash I can get (IE if and when I have kids)

However, I may need to manage my cash flow in the coming months with increases in the cost of living. I currently have a limited margin of error each month and am using my bonus/stock to keep me going. This is not a sustainable long-term solution (especially in a recession!)

If I can maintain pension payments and mortgage payments alone, my net worth (house prices and pension staying at the same value) would increase by £1500 per month.

Downturns are where generational wealth can be made, you need to use the tools available to you. I am choosing to treat myself as poor each month so that I may thrive 10 years from now.

Follow along to find out how I get on.

- Net Worth – September 2022 – 22.40% to FIRE (8.5% yield, and a crashing pound)

It has been a strange month. We’ve had some craziness going on in the UK economy that is pretty painful to watch. Interest rates are coming for us and many in FIRE are concerned that their plans may be thwarted. With interest rates going up, those of us that have mortgages are going to be paying a significant portion of our income to the banks rather than into investments in the market.

I expect the allocation of capital for most with sense to be this, income > savings (high rate) > pay down the principal on mortgages at the end of the current fix. Practically speaking if interest rates are 5-6% I would rather put my money into that (a so-called guaranteed return) and pay down the debt. The market might return 10% but it is not guaranteed, I’d like to take the option with the most certainty in this current environment.

My fix is up for renewal in 2024 August, hopefully, the outlook is clearer and rosier by then.

Net Worth Update

My net worth reached a new high this month: £111,994.61 a mixture of reduced spending, a bonus at work, paying down my mortgage and (the important one) house prices drastically increasing – about £3k). Goes to show, it doesn’t matter what you do, your unearned wealth will probably beat your earned wealth. My cash and savings increased to the north of £1,000 for the first time since 2020 as I try and make sure I have a safety net to fall back on in the coming months.

My savings are in a blend of easy access, and slightly riskier peer-to-peer lending. With a sprinkle stashed in Blockfi. This pays me, 8.5% and is paid out monthly. This is evidently high for a “stable” coin so I’ve only allocated a small amount to this. They are backed by Gemini and this money is returned out of profits, but I would treat it as investing in Coinbase or similar. You don’t make an 8.5% return without ANY risk. I like the hedge as it also pays out in dollars, so is worth a heck of a lot more than at the start of the year. BlockFi is great for someone living in the UK.

Likely to do well long-term, but there is a chance it all blows up as well. This chance is small but please don’t put all your eggs in one basket! Having said all that, you can sign up via my ref link here: https://app.blockfi.com/signup/?ref=005efaf1 or non-referral https://app.blockfi.com

Increasing my savings is the number one priority for now, trying to get as much money aside for the winter months, and for the mortgage refinance in August 2024. This seems like a long time away, but creating a comfortable financial situation will allow me to focus on my building out my various (but very small!) streams of income.

Future Net Worth

Currently increasing my net worth at around 1% of my FIRE target per month, so it should take another 78 months, IE 6.5 years – exactly the age of 35 that I wanted to retire at. However, I don’t see this increasing in the medium term at the same rate as most of my net worth has come from my house. I need to live in it, the cost of borrowing is going up, and the price of my house is likely to go down in the short to medium term. I will reflect that in my monthly newsletter. You may well see a few months of horrific decline on this blog.

Niche Sites Update:

I also launched a new niche site this month, more information to follow. The idea is to focus on certain underserved segments that are not worth the big company’s time, but worth it for a side or full-time personal income. My site is ranking in google, but very low, and a lot more content needs to be generated, not sure if I should go down the path of paying someone or doing it myself.

I guess at some point I will need to learn about backlinks!

If you want to read last months here it is: